Autumn Budget 2018 – Key Tax announcements for Employers

5 Key Tax Announcements that Employers should note:

The Chancellor delivered his 2018 Budget on 29 October 2018. The Autumn Budget 2018 contained several announcements relating to employment taxes, five of which are explored in more detail below:

1. Employment Allowance

2. National living wage and national minimum wage

3. Termination payments

4. Short term business visitors

5. IR35 reform in the private sector

1. Employment Allowance

In 2014, the Government introduced the National Insurance contributions (NIC) employment allowance. This reduces the annual employers’ Class 1 NIC liability of a business by the amount of the employment allowance. The allowance is currently £3,000 per annum but can only be claimed by one entity in a group each year.

The allowance was introduced to help stimulate economic growth by encouraging smaller businesses to take on employees and is currently available to all employers regardless of size.

However, from 6 April 2020 only employers with an employers’ NIC liability of less than £100,000 in the previous tax year will be eligible to claim it.

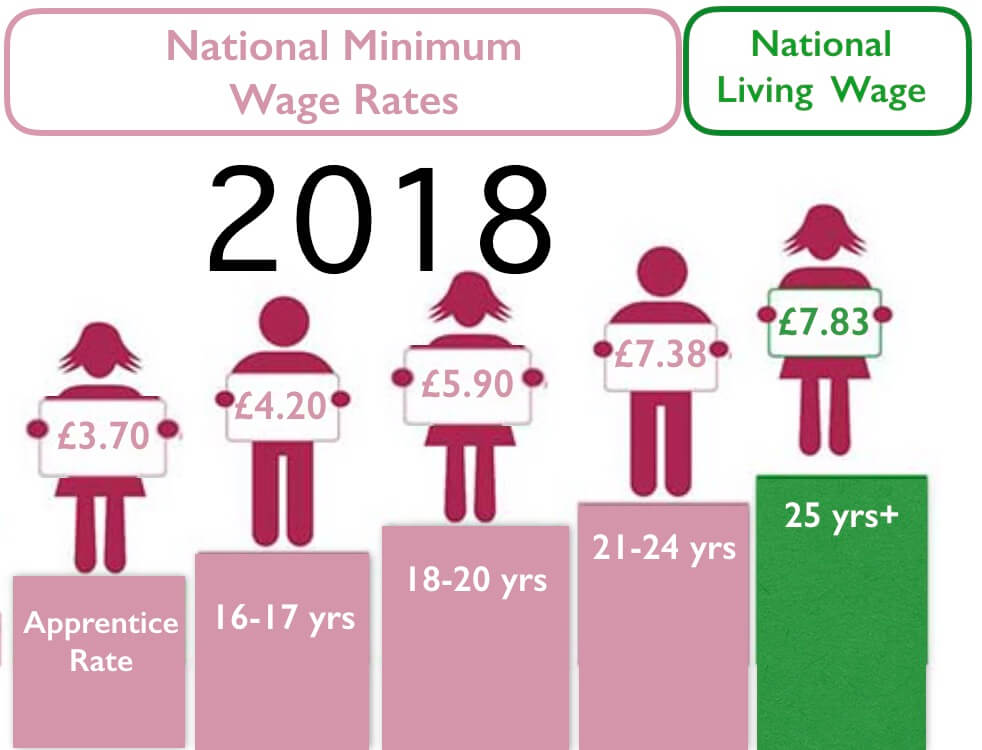

2. National living wage and national minimum wage

There have also been changes to the national living wage and national minimum wage rates.

The national living wage is the statutory minimum wage rate for individuals aged 25 or over. It is currently set at £7.83 an hour but the Chancellor confirmed that this will rise to £8.21 an hour from April 2019… a significant 4.9% increase.

The national living wage is the statutory minimum wage rate for individuals aged 25 or over. It is currently set at £7.83 an hour but the Chancellor confirmed that this will rise to £8.21 an hour from April 2019… a significant 4.9% increase.

The Chancellor also announced increases to the national minimum wage rates, which is relevant for individual aged under 25. In particular, the rate for 21 to 24 year olds is increasing from £7.38 to £7.70 per hour, and the rate for 18 to 20 year olds is rising from £5.90 to £6.15 per hour.

While this is positive news for lower paid employees, it will be a further cost for their employers to absorb. It is not just the additional cost of paying these increased hourly rates which businesses must factor in, as there could be consequential effects on other costs and areas such as:

• employers’ Class 1 NIC liabilities;

• the apprenticeship levy;

• pension contributions under pension auto-enrolment; and

• employees’ ability to participate in salary sacrifice arrangements.

Businesses must continue to be compliant with national living wage and national minimum wage legislation, especially as the rates increase.

3. Termination payments

The Government substantially changed the rules on termination payments with effect from 6 April 2018, particularly in relation to ‘post-employment notice pay’ (PENP), – HMRC has published guidance’.

A further change was expected to take effect from 6 April 2019, whereby the income tax and employers’ NIC rules would be aligned so that employers’ NIC (but not employees’ NIC) would also be due (in addition to tax) on certain termination payments above the £30,000 threshold.

This change will increase employers’ costs in respect of termination packages to departing employees which exceed the £30,000 threshold. The welcome news in the Budget is that this change has been put back by another year and is now anticipated to be effective from 6 April 2020.

4. Short term business visitors

Before the 2015/16 tax year, short-term business visitors (STBVs) visiting the UK from entities in countries which the UK did not have a double tax agreement (DTA) with, or from overseas branches of the UK entity, could not be included in a standard short term business visitors arrangement (STBVA) with HMRC. This meant that the UK business these STBVs were working for had to operate PAYE on the STBV’s earnings in real time.

With effect from the 2015/16 tax year, the Government introduced a special PAYE arrangement for STBVs who could not be included in a standard STBVA but who work in the UK for no more than 30 days in a tax year. Under this arrangement HMRC will set up an annual PAYE scheme for the UK business, which allows it to account for the tax due on the earnings of such STBVs’ which relate to UK workdays after the end of the tax year. A single end of year PAYE return must be delivered to HMRC by 19 April following the end of the tax year, and the tax due must be paid to HMRC by 22 April (if paid electronically).

The Chancellor announced two further welcome improvements to this special PAYE arrangement to take effect from 6 April 2020, namely:

• The UK workday rule is being extended from 30 to 60 workdays, which means that more STBVs coming from entities in countries which the UK does not have a DTA with or from overseas branches of the UK entity, can qualify for this special arrangement.

• The reporting and payment deadlines are being moved from 19 and 22 April to 31 May following the tax year, which will allow the UK businesses more time to gather information and make their returns and payments. It also aligns the special arrangement with the reporting obligations under the STBVA.

5. IR35 Reform in the Private Sector

The IR35 rules were originally introduced in 2000 with the intention of ensuring that individuals who supply their services via an intermediary (such as a personal service company) but would be employees of the end user entity if the intermediary were not used, pay the same tax and NIC an employee would pay.

Under current rules for private sector contracts, the worker’s intermediary must assess and (where appropriate) apply the IR35 rules.

The Chancellor confirmed in his Budget that from 6 April 2020 the rules will change for medium-sized and large businesses in the private sector. From that date, the obligation for assessing whether IR35 applies will fall with the end user of the worker’s services, as it has done for public sector contracts since April 2017. Where it is concluded by the end user that IR35 applies, the fee payer (which may be the end user or an agency etc) will become responsible for accounting for and paying the tax and NIC due to HMRC under PAYE, including the additional cost of employers’ NIC.

The IR35 rules are notoriously complex, and this change could present many private sector businesses with additional, and often substantial, challenges and costs. Preparation for this significant change will therefore be crucial.

{kind=link}